As we go headlong into

2018, I believe UK interest rates will stay low, even

with the additional 0.25% increase that is expected in May or June. That rise will

add just over £20 to the typical £160,000 tracker mortgage, although with 57.1%

of all borrowers on fixed rates, it will probably go undetected by most

buy-to-let landlords and homeowners. I forecast that we won’t see any more

interest rate rises due to the fragile nature of the British economy and the

Brexit challenge. Even though mortgages will remain inexpensive, with retail

price inflation outstripping salary rises, it will still very much feel like a

heavy weight to some Aylesbury households.

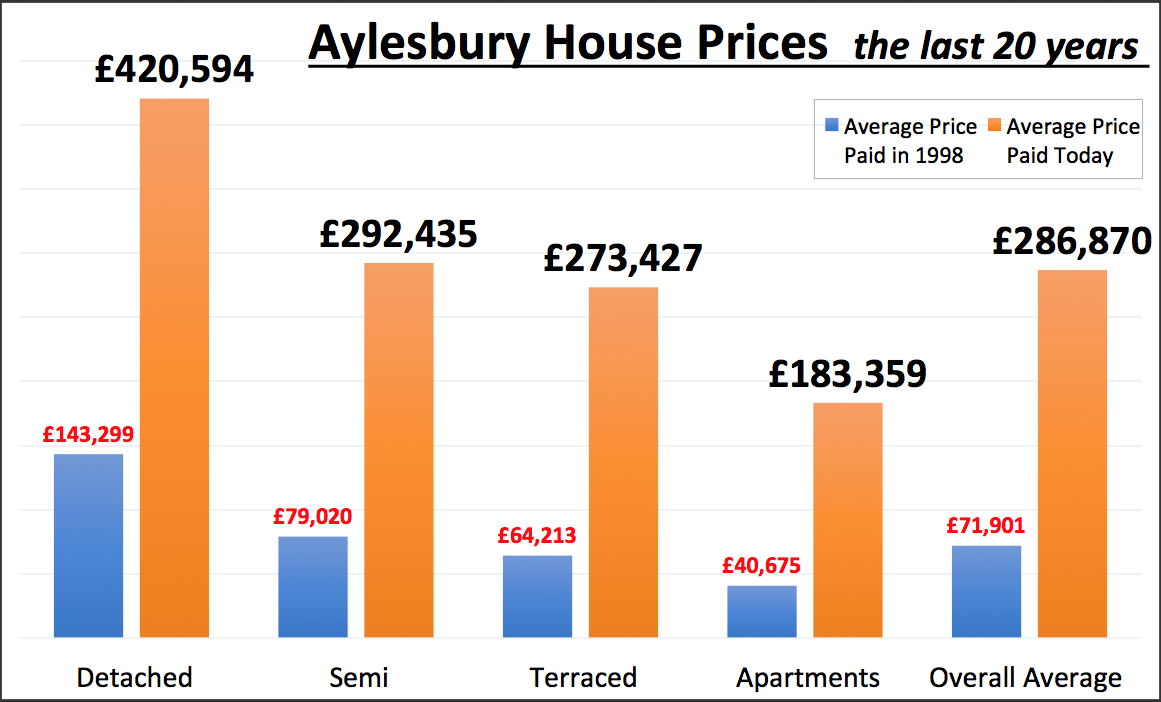

Now it’s certain the Aylesbury

housing market in 2017 was a little more subdued than 2016 and that will

continue into 2018. Property ownership is a medium to long-term investment so looking

at that long-term time frame; the average Aylesbury homeowner who bought their property

20 years ago has seen its value rise by more than 300%.

This is important as

house prices are a national obsession and tied into the health of the UK

economy as a whole. The majority of that historic gain in Aylesbury property

values has come from property market growth, although some of it will have been

added by homeowners modernising, extending or developing their Aylesbury homes.

Taking a look at the

different property types in Aylesbury and the profit made by each type, it

makes interesting reading..

However, I want to put aside all that historic growth and profit

and looking forward to what will happen in the future. I want to look at the

factors that could affect future Aylesbury (and the Country’s) house price

growth/profit; one important factor has to be the building of new homes both

locally and in the country as a whole. This has picked up in 2017 with 217,350

homes coming on to the UK housing ladder in the last year (a 15% increase on

the previous year’s figures of 189,690. However, Philip Hammond has set a

target of 300,000 a year, so still plenty to go!

Another

factor that will affect property prices is my prediction that the balance of

power between Aylesbury buy-to-let landlords and Aylesbury first-time buyers

should tip more towards the local first-time buyers in 2018.

The

Council of Mortgage Lenders expects the number of buy to let mortgages to drop

by 34% from levels seen in 2015. This is because of taxes being increased

recently on buy-to-let and harder lending criteria for buy to let mortgages,

which means I foresee a gradual move in the balance of power in favour of first-time

buyers rather than buy-to-let landlords. First time buyers will also be helped

by The Chancellor eradicating Stamp Duty for all properties up to £300,000

bought by first-time buyers in the recent budget.

This means Aylesbury

buy-to-let landlords will have to work smarter in the future to continue to

make decent returns (profits) from their Aylesbury buy-to-let investment. Even with the tempering of house price inflation in Aylesbury

in 2017, most Aylesbury buy to let landlords (and homeowners) are still sitting

on a copious amount of growth from previous years.

The question is, how

do you, as an Aylesbury buy to let landlord ensure that continues?

Since the 1990’s,

making money from investing in buy-to-let property was as easy as falling off a

log. Looking forward though, with all the changes in the tax regime and balance

of power, making those similar levels of return in the future won’t be as easy.

Over the last ten years, I have seen the role of the forward thinking letting

agents evolve from a ‘rent collector’ and basic property management to a more

holistic role, or as I call it, ‘landlord portfolio strategic leadership’.

Thankfully, along with myself, there are a handful of letting agents in Aylesbury

whom I would consider exemplary at this landlord portfolio strategy where they

can give you a balanced structured overview of your short, medium and long-term

goals, in relation to your required return on investment, yield and capital

growth requirements. If you would like such advice, speak with your current

agent – or whether you are a landlord of ours or not – without any cost or

commitment, feel free to drop me a line.